This Blog has been removed from our site

MAY 26, 2026

“My Property Is Worth More!” — Understanding Commercial Property Valuations in Today’s Marke...

Read More

MARCH 05, 2026

TELKOM NATIONAL PROPERTY DISPOSAL | 60 PROPERTIES ACROSS SOUTH AFRICA

Read More

JANUARY 15, 2026

Momentum Meets Opportunity: In2Assets Sets the Stage for a Record-Breaking 2026

Read More

NOVEMBER 21, 2025

Positive Momentum Surges in KwaZulu-Natal’s Commercial Property Sector as In2Assets Closes Over R2...

Read More

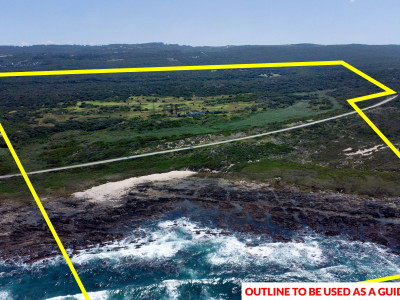

NOVEMBER 19, 2025

Unprecedented Coastal Canvas: In2assets Unveils Rare Eastern Cape Development Site with Private Ocea...

Read More

OCTOBER 14, 2025

Realizing Maximum Value for Durban Harbour Property: Why Auctions Lead the Market

Read More

OCTOBER 09, 2025

Partnership Proven: In2assets Reinforces Long-Standing Broker Collaboration, Driving Superior Commer...

Read More

AUGUST 06, 2025

When Times Get Tough: Why Company Owners Need to Free Up Cash Flow and How Property Auctions Provide...

Read More

JULY 11, 2025

The Unseen Foundation: Why Valuation is Key to Auction Success and the Secrecy of the Reserve Price

Read More